After several years of significant adjustments, the global lithium-ion battery industry reached a critical turning point in the second half of 2025. Entering 2026, the industry stands at a crossroads between old and new cycles: on one side, strong demand driven by the surge in energy storage; on the other, supply constraints caused by capacity rationalization and dramatic policy changes. Considering various factors such as raw material costs, global trade policies, geopolitics, and supply and demand dynamics, let’s examine the price trends of lithium-ion batteries over the next two years.

Raw Material Costs Bottom Out and Rebound

Over 70% of the cost of lithium-ion batteries stems from materials, with the prices of key metals such as lithium, cobalt, and nickel being decisive factors.

1. Lithium Carbonate

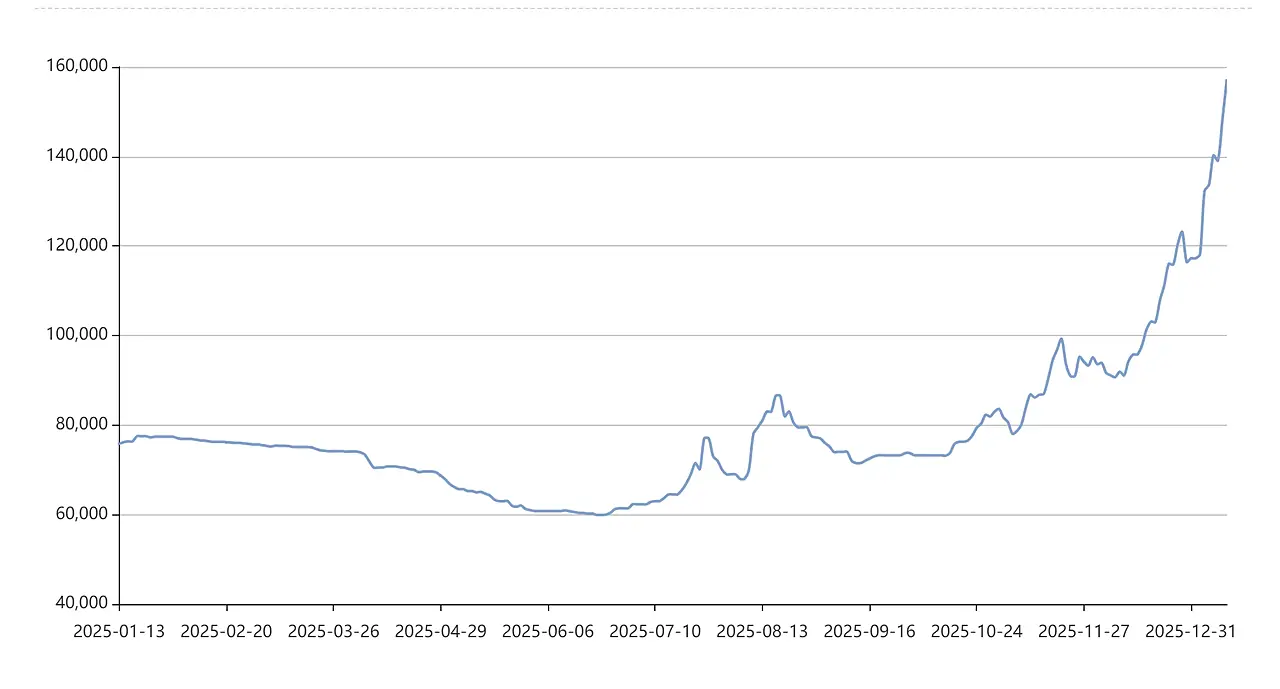

As the “white oil,” lithium carbonate prices bottomed out in June 2025 (around ¥59,000/ton) before staging a strong rebound, surpassing ¥130,000/ton by the end of 2025—doubling within six months. This surge was primarily driven by the explosive growth in energy storage demand exceeding expectations and the ongoing destocking across the supply chain. Looking ahead to 2026-2027, while market assessments of lithium prices vary, consensus holds that the price floor has significantly risen.

Industry institutions generally predict that the market will be in a state of “tight balance” by 2026. On one hand, demand for energy storage and power continues to grow; on the other hand, capital expenditures remain low following prolonged industry losses, limiting supply elasticity. Market expectations indicate that the average price of battery-grade lithium carbonate will fluctuate significantly within a core range of 80,000 to 150,000 yuan per ton throughout the year.

For 2027, institutions show increasing divergence in their outlook for lithium-ion battery trends, yet expectations of shortages are beginning to intensify. The critical factor lies in whether the high prices expected in 2026 will sufficiently stimulate large-scale new capacity additions. If not, as demand continues to grow, global lithium supply and demand could shift toward a shortage in 2027. This anticipated future shortage is likely to be reflected in prices as early as the second half of 2026, driving prices to challenge higher price ranges.

2. Key Auxiliary Materials: Cobalt and Nickel

Cobalt: Its pricing has moved beyond pure supply-demand dynamics, entering a “policy-driven” phase. Export quota controls imposed by the Democratic Republic of Congo (DRC), the world’s largest cobalt producer, will drive cobalt prices to surge over 300% by 2025. With export quotas remaining tight in 2026 and low circulating inventories across the supply chain, cobalt prices are more likely to rise than fall, expected to trade within a high range of $24–29 per pound. This will provide rigid support for ternary (NCM/NCA) battery costs.

Nickel: The situation is the opposite of cobalt, facing structural oversupply pressure. However, policy interventions by Indonesia—the largest producer—such as controlling mining quotas, have established a “policy floor” for nickel prices. The main Shanghai nickel contract is expected to fluctuate between 110,000 and 140,000 yuan per ton, with a low probability of falling below the cost line. This implies that nickel prices will have a limited drag on battery costs.

3. Midstream Materials

After enduring prolonged industry-wide losses, key components such as cathodes (e.g., lithium iron phosphate) and electrolytes (with lithium hexafluorophosphate as the core solute) have seen strong price hike demands. For instance, lithium hexafluorophosphate prices surged by 150%-200% in the second half of 2025. Against a backdrop of improving demand, the price recovery of midstream materials will continue to cascade toward the battery segment, becoming a direct driver of rising battery costs.

Policy Variable

In early 2026, a far-reaching policy was officially finalized: China announced that starting April 1, 2026, the export VAT rebate rate for battery products would be reduced from 9% to 6%, with plans to eliminate it entirely effective January 1, 2027. This will have a profound impact on the export performance of China’s battery industry.

1. Direct Impact

The cancellation of tax rebates directly increases export costs for Chinese battery manufacturers by 6% to 13%. This widespread increase in “China costs” will inevitably be reflected in the pricing of exported batteries. Following the policy announcement, lithium carbonate futures surged 9% in a single day, triggering a sharp market reaction.

2. Short-term Effects

The policy has established a transition period ending in 2026, which may trigger concentrated orders from domestic and international buyers. Manufacturers are rushing to export to take advantage of the final tax rebate benefits. This front-loading of demand will intensify market supply constraints in the short term, further driving up raw material and battery prices in the first half of 2026.

3. Long-term Effects

In the long run, this will accelerate the elimination of inefficient capacity in China’s lithium battery industry and compel leading companies to expedite local manufacturing facilities overseas—such as in Europe and Southeast Asia—to circumvent tariffs and cost pressures. The global battery supply chain will shift from “Made in China, consumed globally” to “Manufactured globally, consumed regionally.”

Market Barriers

While China proactively adjusts its policies, other national markets are erecting stricter technical and trade barriers, thereby impacting price structures and flow patterns.

The EU’s New Battery Law represents the world’s most stringent battery access regulations. Compliance demands substantial improvement investments, directly increasing the cost of batteries exported to Europe. The U.S. Inflation Reduction Act (IRA) heavily favors “North American-made” batteries and critical minerals through massive subsidies. Simultaneously, U.S. tariffs on Chinese electric vehicles, batteries, and raw materials remain in effect. The combined impact of these measures will create significant regional disparities in battery pricing.

Beginning in 2026, air transport costs and complexities for lithium batteries will increase. Concurrently, global regulations on safety, recycling, and other aspects are tightening. These ubiquitous compliance requirements are quietly elevating the total lifecycle cost of batteries.

Demand and Supply

1.Demand

The surge in energy storage is pivotal to reversing expectations for the lithium battery industry. China’s refined capacity-based electricity pricing policy has established a stable revenue model for energy storage projects, while the global energy transition has created massive demand for grid flexibility resources. Industry forecasts indicate that global energy storage battery shipments could grow by over 50% by 2026, with its demand for lithium potentially far outpacing that of electric vehicles.

In contrast, the power market may see slowing growth in global EV sales volume. However, increased battery capacity per vehicle (driven by larger, higher-end models) and the rapid penetration of new energy commercial vehicles—particularly electric heavy-duty trucks—provide additional, robust growth momentum.

2. Supply

The industry has endured three years of losses, with capital expenditures now at low levels. Current capacity expansion efforts are primarily concentrated among leading companies, and the cycle from investment to production ramp-up requires at least 1-2 years. Consequently, new effective capacity additions will be limited in 2026-2027.

Most material segments currently operate at around 70% capacity utilization, still below full recovery levels. Against the backdrop of the entire industry just achieving modest profit recovery, companies lack the incentive to pursue large-scale expansions that could reignite price wars.

Summary

From 2026 to 2027, lithium-ion battery prices are projected to experience an overall upward trend with volatility. Driven by rising raw material costs, adjustments to China’s export policies, and surging demand for energy storage, prices are more likely to increase than decrease.

Specifically, prices are expected to follow a pattern of rising first and then falling, with the overall price level shifting upward. Meanwhile, significant price divergence will emerge among products across different regions and technological approaches.

In summary, the 2026-2027 lithium battery market is transitioning away from the old cycle reliant on subsidies and reckless expansion, entering a new phase defined by genuine demand, global compliance, and cost-value alignment. The rise in battery prices fundamentally reflects a repositioning and return to its core value as the “new energy infrastructure.”